UK Basel 3.1: Credit valuation adjustment and counterparty credit risk

On 12 December 2023, the Prudential Regulation Authority (PRA) published near-final rules on the implementation of Basel 3.1 standards through Policy Statement 17/23 (PS17/23) which offers feedback on the responses received for Consultation Paper 16/22 (CP16/22) published on 30 November 2022.

The implementation date for Basel 3.1 standards is July 1, 2025.

A summary of the key changes to the calculation of Credit valuation adjustment and counterparty credit risk is provided below.

Key changes include:

Credit valuation adjustment (CVA) risk:

Three new methodologies have been introduced to replace the current framework:

Alternative Approach (AA-CVA): Available to firms with limited non-centrally cleared derivatives

Basic Approach (BA-CVA): Available to all firms

Standardised Approach (SA-CVA): Available with prior permission from the PRA. In addition, an annual attestation is required confirming that the firm continues to meet the requirements to use this approach.

Firms may use a combination of BA-CVA and SA-CVA, however, firms using AA-CVA would not be able to use any other approach simultaneously.

The scope of application of the CVA risk framework increased to include exposures to sovereigns, non-financial counterparties, and pension funds.

Counterparty credit risk (CCR):

Under the standardised approach to counterparty credit risk (SA-CCR) framework, the ‘alpha factor’ has been reduced from ‘1.4’ to ‘1’ for exposures to pension funds and non-financial counterparties.

A summary of the revised approaches is given below:

Approaches:

Out of the available methods outlined above, two methods seem appropriate for banks with limited exposure in derivatives, these are the Alternative Approach (AA-CVA) and the reduced version of the Basic Approach (BA-CVAreduced). BA-CVAreduced is relevant for firms that do not hedge CVA risk.

AA-CVA: This approach may be used by a firm with over-the-counter (OTC) derivatives of a notional aggregate amount of less than £88 billion. The firm needs to notify the PRA before using this approach.

In AA-CVA, no separate calculation is required to determine the own funds requirements for CVA risk, it would be equal to the own funds requirements for counterparty credit risk. In other words:

Own funds requirements for CVA risk = Own funds requirements for counterparty credit risk.

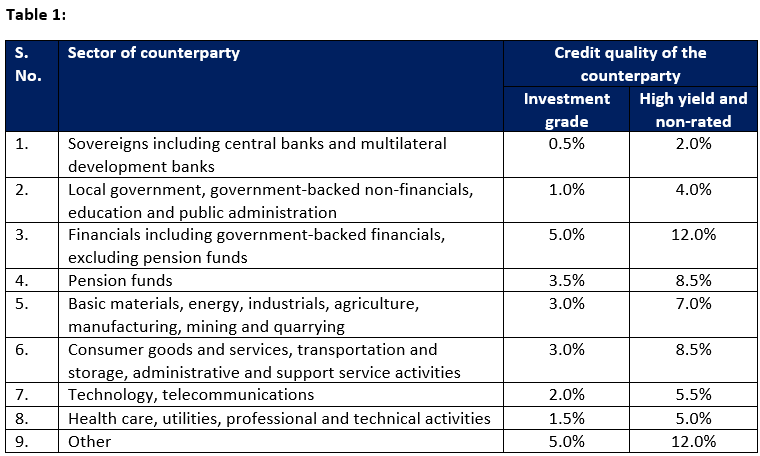

BA-CVAreduced: A firm should calculate its own funds requirements for CVA risk under this approach using the following formula:

CVA own funds requirement calculation: an example for AA-CVA and BA-CVAreduced approaches

The following two netting sets and associated counterparty credit risk (CCR) data points are considered as input for this example:

Own funds requirement under AA-CVA:

No separate calculation is required under AA-CVA. The own funds requirement under this approach would be equal to the own funds requirement under CCR i.e. £700.

Own funds requirement under BA-CVAreduced: