UK Basel 3.1: Credit risk standardised approach – exposures to multilateral development banks (MDBs)

On 12 September 2024, the Prudential Regulation Authority (PRA) published the second part of its near-final rules on the implementation of Basel 3.1 standards through Policy Statement 9/24 (PS9/24) which offers feedback on the responses received on Consultation Paper 16/22 (CP16/22) published on 30 November 2022.

PS9/24 covers inter alia the near-final rules on credit risk, disclosures, and reporting as well as minor clarifications and corrections to the previous near-final rules published within PS17/23. The implementation date for Basel 3.1 standards has now been postponed to 1 January 2027.

A summary of the changes relating to ‘exposures to multilateral development banks’ (MDBs) under the credit risk standardised approach is provided below.

Key changes to exposures to MDBs, under the standardised approach, include:

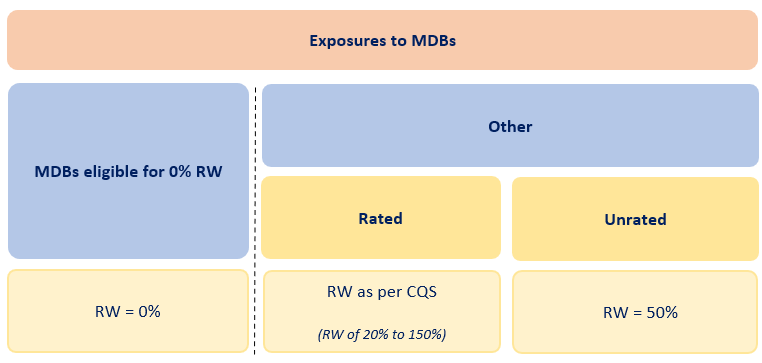

Risk weights as per CQS are introduced for externally rated MDBs (excluding those MDBs already eligible for a 0% risk weight).

A risk weight of 50% would apply to unrated MDBs.

A summary of the revised classifications and applicable risk weights is given below:

Existing and revised risk weights

How We Can Help

Banks may face a variety of challenges when preparing for Basel 3.1. At Katalysys, we have a deep understanding of prudential regulatory requirements both from the perspective of rules and practical implementation. Our team is already supporting a range of clients in this area, and includes:

Workshops or training to cover new requirements.

Gap and impact analyses.

Guidance on implementing industry best-practice in relation to the Basel 3.1 standards.

Documenting or updating assumptions and interpretations in regulatory reporting.

Preparation of regulatory reporting policies and procedure notes.

Validation of the system outputs and calculations.

Review of regulatory returns, including post-implementation of Basel 3.1 changes.

For more information, please contact:

Josh Nowak

Managing Director, Risk & Regulatory Consulting

T: +44 (0)7587 720 988

Manish Patidar

Director, Regulatory Consulting

T: +44 (0)7766 001 643